VAT Invoice vs Regular Invoice: Key Differences

Understanding the distinction between a VAT invoice and a regular invoice is critical for compliance. A VAT invoice is a statutory tax document that enables input tax recovery, while a regular invoice is simply a commercial record of a transaction.

| Feature | Regular Invoice | VAT Invoice |

|---|---|---|

| VAT Registration Number | Not required | Mandatory |

| Tax Breakdown | Not required | Must show VAT rate & amount separately |

| Customer VAT Number (B2B) | Optional | Required for cross-border |

| Legal Status | Commercial document | Statutory tax document |

| Input Tax Recovery | Not possible | Enables VAT reclaim |

8 Mandatory VAT Invoice Fields (Global Standard)

While local nuances exist, the OECD and major tax directives align on these 8 core data points required for a document to be considered a valid VAT invoice. Missing any of these fields can invalidate your invoice for tax recovery purposes.

| Data Attribute | Compliance Requirement |

|---|---|

| 1. Sequential Invoice ID | Must be unique and sequential. Gaps in numbering sequences trigger audit flags for suppressed income. |

| 2. Time of Supply (Tax Point) | The date the transaction occurred legally, which determines the VAT return period. |

| 3. Supplier Tax Identity | Full Legal Name, Registered Address, and VAT/GST/ABN Number. |

| 4. Customer Tax Identity | Mandatory for B2B transactions, especially for Cross-Border/Reverse Charge validation. |

| 5. Line Item Specifics | Detailed description of goods/services (generic terms like "Consulting" are often rejected). |

| 6. Net Value (Pre-Tax) | The taxable amount per line item, expressed in the supplier's functional currency. |

| 7. Applied Tax Rate & Amount | The exact tax value. In multi-currency invoices, the Tax Amount must be converted to the supplier's local currency. |

| 8. Total Gross Amount | The final payable sum (Net + Tax). |

Simplified VAT Invoice (UK: Under £250)

In the UK, HMRC allows a simplified VAT invoice for retail sales under £250 (including VAT). This reduces the mandatory requirements and streamlines transactions for small purchases. For general invoice structure guidance, see our payment terms guide.

Simplified Invoice Must Include:

- Supplier's name and address

- Supplier's VAT registration number

- Date of supply (tax point)

- Description of goods/services

- Total amount payable (including VAT)

- VAT rate applied

Can Be Omitted:

- Customer's name and address

- Unique invoice number (though still recommended)

- Separate VAT amount calculation

Note: Simplified invoices are primarily used in retail environments. For B2B transactions or amounts over £250, a full VAT invoice is required. You can generate a compliant VAT invoice using our free tool.

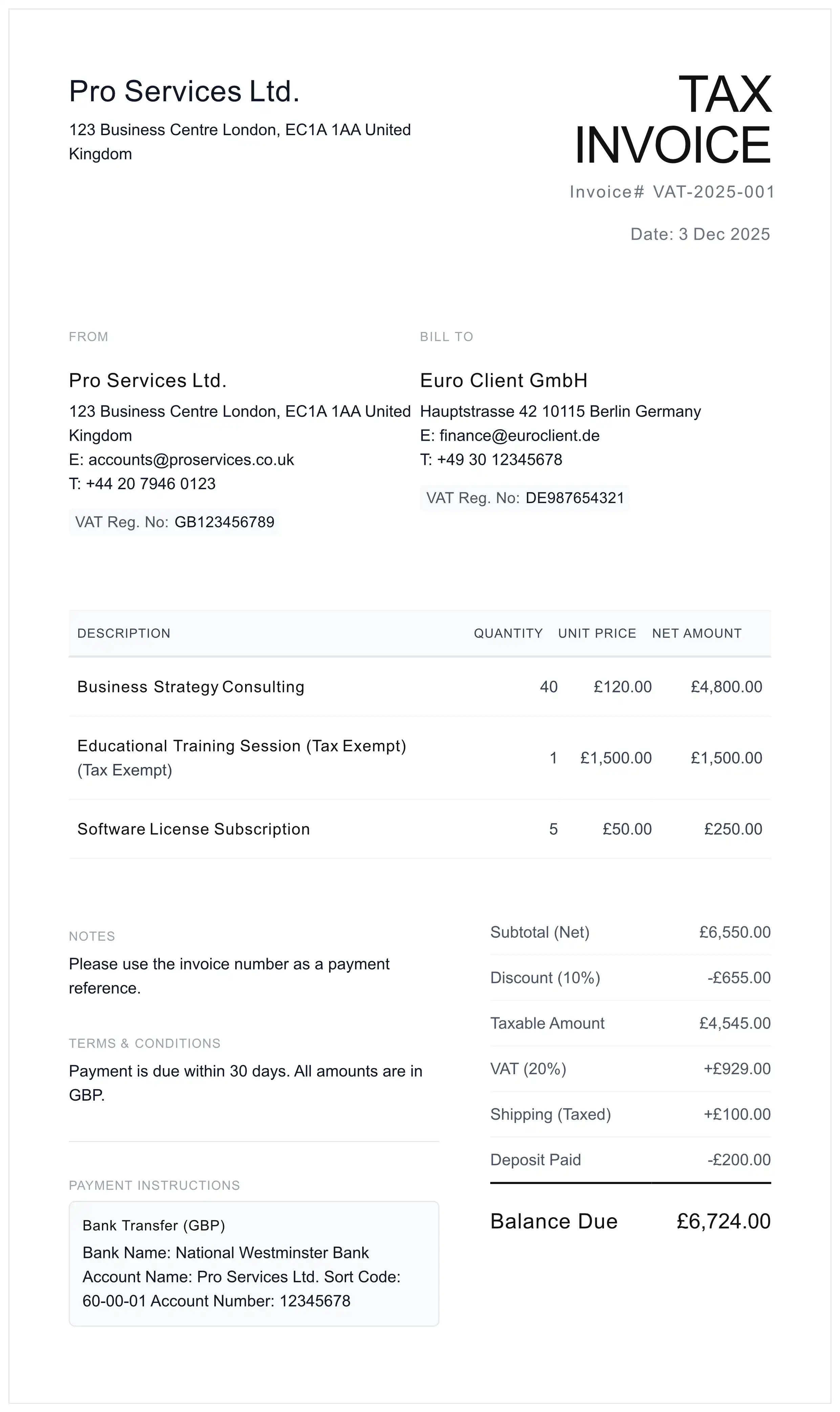

Anatomy of a Compliant Invoice

The visual structure of an invoice must facilitate rapid auditing. Below is an example generated by our system that separates tax components to meet strict accounting standards.

Country-Specific VAT Rules: UK, EU, Australia & Canada

Compliance is location-dependent. Below are the critical references for major jurisdictions as of 2026. For cross-border goods shipments, also see our Commercial Invoice Guide for customs documentation requirements.

UK VAT Invoice Requirements

The UK VAT system is governed by HMRC (Her Majesty's Revenue and Customs) and follows the Value Added Tax Act 1994. All VAT-registered businesses must issue compliant invoices under HMRC VAT Record Keeping rules.

- Standard VAT Rate: 20% (reduced rate: 5%, zero rate: 0%).

- Simplified Invoice Threshold: Allowed for retail sales under £250 (including VAT). Simplified invoices require fewer fields -- no customer name/address and no separate VAT amount calculation needed.

- Making Tax Digital (MTD): Since April 2022, all VAT-registered businesses must maintain digital records and submit VAT returns through MTD-compatible software. Handwritten or manual invoices are effectively obsolete for compliance purposes.

- Invoice Time Limit: Must be issued within 30 days of the date of supply (tax point).

- Currency: If invoicing in a foreign currency, the VAT amount must be converted to GBP using HMRC's published exchange rate for the date of supply.

- Record Retention: VAT records, including invoices, must be kept for at least 6 years.

EU VAT Invoice Requirements

EU VAT invoicing is harmonized under Council Directive 2006/112/EC, though member states may add local requirements. The EU is actively transitioning to digital invoicing through the ViDA (VAT in the Digital Age) initiative.

- Directive 2006/112/EC: Establishes the minimum mandatory fields for all VAT invoices within the EU, including both parties' VAT identification numbers, sequential invoice number, date of supply, and a line-by-line tax breakdown.

- Reverse Charge Mechanism: For intra-Community B2B supplies, the supplier issues an invoice at 0% VAT with the notation "Reverse Charge applies." The buyer self-assesses VAT in their own country. Both VAT numbers must be validated via VIES (VAT Information Exchange System).

- ViDA (VAT in the Digital Age): The EU's ViDA proposal mandates real-time digital reporting for intra-EU B2B transactions. By July 2030, all cross-border B2B invoices must be issued electronically in a structured format (EN 16931). Member states are already implementing national e-invoicing mandates ahead of this deadline.

- Intra-Community Supply: Goods shipped between EU member states are zero-rated for the seller, provided the buyer's VAT number is valid and the goods physically leave the origin country. Proof of transport is required.

- Language: Invoices can be issued in any language, but tax authorities may request a certified translation during an audit.

- Self-Billing: The EU permits self-billing arrangements where the buyer issues the invoice on behalf of the supplier, provided both parties agree in advance.

Australian GST Invoice Requirements

Australia's Goods and Services Tax (GST) is administered by the ATO (Australian Taxation Office) at a flat rate of 10%. The rules for tax invoices are defined under the A New Tax System (Goods and Services Tax) Act 1999.

- Tax Invoice Threshold: A valid tax invoice is required for GST credits on purchases of $82.50 AUD or more (GST-inclusive). Below this threshold, a simplified receipt may suffice.

- Tax Invoice vs Adjustment Note: A tax invoice documents the original sale. An adjustment note (similar to a credit note) is required when the price, GST, or quantity changes after the original invoice was issued. Adjustment notes must reference the original tax invoice number.

- Buyer ABN Requirement: For sales over $1,000 AUD, the buyer's identity and ABN (Australian Business Number) must appear on the tax invoice.

- Regulation: Full rules are published by the ATO Tax Invoices page.

- GST-Free Supplies: Certain supplies (exports, medical, education) are GST-free. These must still appear on the tax invoice but marked at 0% GST.

- E-Invoicing: Australia adopted the Peppol framework for B2G (business-to-government) e-invoicing since July 2022 and is expanding to B2B adoption.

- Record Retention: Tax invoices and records must be kept for 5 years from the date the return was lodged.

Canadian GST/HST Invoice Requirements

Canada's indirect tax system is administered by the CRA (Canada Revenue Agency) and combines federal GST with provincial sales taxes. The rules vary significantly depending on the province of supply.

- GST vs HST vs PST: Five provinces use HST (Harmonized Sales Tax) which combines federal GST and provincial tax into one rate: Ontario (13%), Nova Scotia (14%), New Brunswick (15%), Newfoundland & Labrador (15%), and Prince Edward Island (15%). Other provinces charge GST (5%) federally plus their own PST (Provincial Sales Tax) separately (e.g., British Columbia: 5% GST + 7% PST; Quebec: 5% GST + 9.975% QST).

- Business Number (BN): The supplier's 15-character BN (including the RT program identifier) is mandatory on all invoices for Input Tax Credit (ITC) claims.

- Invoice Tiers by Amount:

- Under $100: supplier name, date, total amount payable are sufficient.

- $100 to $149.99: must also include supplier BN and terms of payment.

- $150 and above: full invoice with buyer name, description of goods/services, and tax breakdown required.

- Tax Breakdown: Invoices must clearly separate GST/HST from PST/QST. The combined amount cannot be shown as a single line for ITC purposes.

- Place of Supply Rules: The tax rate depends on the province where the goods are delivered or the service is performed, not where the supplier is located.

- ITC Claims: Businesses must have a valid invoice with the supplier's BN to claim Input Tax Credits. The CRA can deny ITC claims if the invoice does not meet documentation requirements.

VAT & GST Standard Rates by Country (2026)

The standard rate is what goes on an ordinary B2B or B2C invoice unless the supply qualifies for a reduced, zero or exempt treatment. Every rate below was verified against the official source linked in the same row — the national tax authority or the European Commission — so you can confirm the figure yourself before invoicing. Each row has its own anchor (for example #germany or #united-kingdom), so you can link a colleague straight to one country.

| Country | Tax | Standard rate | Reduced rates | Official source |

|---|---|---|---|---|

| Australia | GST | 10% GST 10% unchanged since 1 Jul 2000; reg threshold AUD 75,000. ATO site blocked WebFetch (403), so cited business.gov.au which states the 10%. | 0% GST-free (basic food, health, education, exports) | business.gov.au (Australian Government) |

| Austria | VAT | 20% Official page (updated 1 Jan 2026): 20% standard, 10%/13% reduced. Announced 5% food rate from 1 Jul 2026 not yet on this page; hygiene items exempt 2026. | 13% / 10% | USP.gv.at (Austrian Business Service Portal, BMF) |

| Bahrain | VAT | 10% Standard 10% since 1 Jan 2022 (doubled from 5%; VAT introduced Jan 2019). Rate stated on the national portal VAT page. | 0% (zero-rated) and exempt on certain goods/services (see NBR) | Bahrain National Portal (bahrain.bh) / NBR |

| Belgium | VAT | 21% Official SPF Finances page: 21% standard, 12% intermediate, 6% reduced, 0% in some cases. Reduced rate on hotels/takeaway meals rises 6%->12% from 1 Mar 2026. | 12% / 6% / 0% | SPF Finances (finances.belgium.be) |

| Bulgaria | VAT | 20% Standard 20%, reduced 9% (hotels, books, baby/hygiene goods - made permanent). 9% on restaurants/bread expired 1 Jan 2025. No change announced for 2026. | 9% / 0% | EC Your Europe (official EU portal) |

| Canada | GST/HST | 5% (federal GST) Federal GST 5% nationwide; HST provinces add provincial part (PEI page: 5% fed + 10% = 15%). NS cut to 14% on 1 Apr 2025. canada.ca blocked WebFetch (403). | HST 13% ON / 14% NS / 15% NB,NL,PEI; GST-only AB,BC,SK | Government of Prince Edward Island |

| Croatia | VAT | 25% Tax Admin page states VAT rates 0%, 5%, 13%, 25% (Art. 38 VAT Act). Standard 25% (one of EU's highest). Rates unchanged for 2026; tax called PDV locally. | 13% / 5% / 0% | Porezna uprava (Croatian Tax Administration) |

| Cyprus | VAT | 19% Standard 19% unchanged; reduced 9%/5%, super-reduced 3%, plus 0% on some essentials extended to end-2026. Cyprus Tax Dept (mof.gov.cy) page was unreachable. | 9% / 5% / 3% / 0% | EC Your Europe (VAT rates table) |

| Czech Republic | VAT | 21% Gov portal: basic rate 21%, reduced 12%. The 2024 consolidation merged old 15%+10% into single 12%; a 0% rate applies to books/medicines. No 2026 change. | 12% / 0% | portal.gov.cz (Czech Government Portal) |

| Denmark | VAT | 25% Single 25% rate, highest in the EU; no domestic reduced rate (only 0% on exports/intra-EU). Locally called 'moms'. Stable, no change announced. | 0% (exports/intra-EU only) | Skattestyrelsen (skat.dk) |

| Estonia | VAT | 24% Standard rate rose 22%->24% on 1 Jul 2025 (now permanent). Reduced: 13% accommodation, 9% books/press/medicines. Locally 'kaibemaks'. | 13% / 9% / 0% | Estonian Tax and Customs Board (EMTA) |

| Finland | VAT | 25.5% Standard 25.5% since 1 Sep 2024 (was 24%). Reduced rate cut 14%->13.5% on 1 Jan 2026 (food, transport, books, medicine); 10% on newspapers. | 13.5% / 10% / 0% | Finnish Tax Administration (Vero) |

| France | VAT | 20% Official BOFiP confirms five rates: 20% normal, 10% and 5.5% reduced, 2.1% particular (super-reduced). 5.5% on gas/electricity subscriptions removed Aug 2025. | 10% / 5.5% / 2.1% | BOFiP - impots.gouv.fr (DGFiP official bulletin) |

| Germany | VAT | 19% EC official table lists DE 19% standard, 7% reduced (USt/MwSt, sec.12 UStG). From 1 Jan 2026 restaurant/catering food permanently at 7%; standard 19% unchanged. | 7% | EC Your Europe (official EU VAT rates table) |

| Greece | VAT | 24% Mainland 24% (since 1/6/2016), reduced 13%, super-reduced 6%. Reduced island rates 17/9/4 expanded to ~24 islands from 1 Jan 2026 (Law 5246/2025). | 13% / 6% (islands 17/9/4) | AADE (Greek tax authority) |

| Hungary | VAT | 27% NAV doc: general rate 27% (highest in EU), preferential 18%, 5% and 0% (daily newspapers). Locally called AFA. No standard-rate change for 2026. | 18% / 5% / 0% | NAV (Hungarian Tax & Customs Administration) |

| India | GST | 5-40% (multi-slab) GST 2.0 (56th Council) cut slabs to 5%/18% + 40% special from 22 Sep 2025 (12%/28% removed). Confirmed via PIB/gstcouncil.gov.in; pages blocked direct fetch, hence medium. | 0% / 5% merit / 18% standard / 40% sin-luxury | GST Council / PIB (Govt of India) |

| Ireland | VAT | 23% Standard 23% since 2012 (page effective 1 Jan 2026). Restaurant/catering & hairdressing drop from 13.5% to 9% from 1 Jul 2026. | 13.5% / 9% / 4.8% / 0% | Revenue (Irish Tax and Customs) |

| Italy | VAT | 22% Standard IVA 22%; reduced 10%, super-reduced 5% and 4%. Rates stable for 2026. Agenzia page confirms 22% standard and 4% reduced (MOSS context). | 10% / 5% / 4% | Agenzia delle Entrate |

| Japan | Consumption Tax | 10% Standard 10% (incl 2.2% local) and reduced 8% (incl 1.76% local) since 1 Oct 2019; no 2026 change. NTA index was nav-only; JETRO gov page states rates. | 8% (food, non-alcohol bev, subscription papers) | JETRO (Japan External Trade Org, go.jp) |

| Kuwait | VAT | No VAT No VAT as of Jun 2026; GCC framework still under parliamentary discussion, draft law in prep. 5% expected eventually. No live Kuwait .gov page found stating status. | — | PwC Worldwide Tax Summaries (Kuwait) |

| Latvia | VAT | 21% Standard 21% confirmed on VID; 12% fresh produce, 5% books/media. Pilot 12% on basic foods (bread, milk, eggs, poultry) runs 1 Jul 2026-30 Jun 2027. 'PVN'. | 12% / 5% / 0% | Valsts ienemumu dienests (VID) |

| Lithuania | VAT | 21% Standard 21% confirmed on VMI. From 1 Jan 2026 old 9% reduced rate became 12% (accommodation/transport/culture); books & medicines cut to 5%. 'PVM'. | 12% / 5% / 0% | Valstybine mokesciu inspekcija (VMI) |

| Luxembourg | VAT | 17% Official AED portal: four rates 17% normal, 14% intermediate, 8% reduced, 3% super-reduced. Lowest EU standard rate. 2023 temporary 16% expired end-2023, back to 17%. | 14% / 8% / 3% | Portail de la fiscalite indirecte (pfi.public.lu, AED) |

| Malta | VAT | 18% Standard 18% (lowest EU after Luxembourg); reduced rates 12%, 7%, 5% and 0%. Confirmed on MTCA official page (footer dated 2026); stable. | 12% / 7% / 5% / 0% | Malta Tax & Customs Admin (MTCA) |

| Netherlands | VAT | 21% Official Belastingdienst page: 3 tariffs 21% high, 9% low, 0%. From 1 Jan 2026 overnight accommodation (hotels/B&B) moved 9%->21%; standard rate unchanged. | 9% / 0% | Belastingdienst (Dutch Tax Administration) |

| New Zealand | GST | 15% Official IRD page states 'GST is charged at a rate of 15%'. Rate unchanged since 1 Oct 2010; no change announced for 2026/27. | 9% (accommodation 28+ days) / 0% (exports) | Inland Revenue (IRD) |

| Norway | VAT | 25% Standard 25% for 2026 (page year-selector set to 2026); 15% on foodstuffs/water-wastewater, 12% on passenger transport, accommodation, cinema. Norway is non-EU. | 15% / 12% | Skatteetaten (Norwegian Tax Administration) |

| Oman | VAT | 5% Standard 5% since 16 Apr 2021 (GCC framework). Official Oman Tax Authority portal states 'Basic rate: 5%'. No rate change announced for 2026. | 0% (exports, 513 essential goods); exempt financial/rent | Oman Tax Authority (Tax Portal) |

| Poland | VAT | 23% MoF: standard 23% (since 2011), reduced 8% and 5%, plus 0% (exports/intra-EU). Page updated 15.12.2025. No standard-rate change for 2026. | 8% / 5% / 0% | podatki.gov.pl (Polish Ministry of Finance) |

| Portugal | VAT | 23% Mainland 23% standard, 13% intermediate, 6% reduced. Azores 16/9/4, Madeira 22/12/5. From Jan 2026 more items moved to 6%; standard unchanged. | 13% / 6% (Azores 16/9/4; Madeira 22/12/5) | gov.pt (Portuguese Government) |

| Qatar | VAT | No VAT No VAT in force as of Jun 2026. GTA laws page lists income/excise/GMT/CGT laws but no VAT law. 5% expected under GCC framework; no official launch date set. | — | Qatar General Tax Authority (GTA) |

| Romania | VAT | 21% Law 141/2025: from 1 Aug 2025 standard rose 19%->21%, single reduced 11% (replaced 5%/9%). Transitional 9% on homes <=120sqm/<=600k lei until 31 Jul 2026. | 11% (9% housing to 31 Jul 2026) | ANAF (Romanian Tax Administration) |

| Saudi Arabia | VAT | 15% Standard 15% since 1 Jul 2020 (raised from 5%). ZATCA eServices page references the 15% rate; PwC VAT chart confirms 15%. No change announced. | 0% (exports/intl transport); exempt financial & real estate | ZATCA (Zakat, Tax and Customs Authority) |

| Singapore | GST | 9% MOF page confirms history: 8% in 2023, 9% in 2024. Now 9%; no further rise announced. IRAS rate pages were JS-rendered (nav only). | 0% (exports, qualifying international services) | Ministry of Finance (MOF) |

| Slovakia | VAT | 23% Standard rate raised from 20% to 23% on 1 Jan 2025; reduced rates 19% (food/electricity) and 5% (medicines, books, accommodation). Official page is Slovak-only. | 19% / 5% | Financna sprava SR |

| Slovenia | VAT | 22% FURS English page confirms 22% general + 9.5% reduced. 5% special rate (books/periodicals) confirmed via FURS Stopnje_DDV doc, not on this English page. | 9.5% / 5% | FURS (Financial Administration of Slovenia) |

| Spain | VAT | 21% General IVA 21%; reduced 10%, super-reduced 4%, plus 0% on some items. Stable; electricity reportedly returned to a reduced rate in Mar 2026 (sub-item only). | 10% / 4% / 0% | Agencia Tributaria |

| Sweden | VAT | 25% Standard 25%. Skatteverket confirms food VAT drops 12%->6% from 1 Apr 2026 (temp, through Dec 2027); restaurant dine-in stays 12%; 6% books/press/transport. 'moms'. | 12% / 6% | Skatteverket |

| Switzerland | VAT | 8.1% Standard 8.1% since 1 Jan 2024; reduced 2.6%, accommodation 3.8%. Planned rise to 8.8% (13th AHV pension) delayed from 2026 to 2028 at earliest. | 2.6% / 3.8% (accommodation) | ESTV / Swiss Federal Tax Administration (FTA) |

| United Arab Emirates | VAT | 5% Standard 5% since 1 Jan 2018; unchanged. Official FTA VAT page shows 5%. Mandatory B2B/B2G e-invoicing phasing in from Jul 2026 (rate unaffected). | 0% / exempt (some financial, residential property) | Federal Tax Authority (FTA) |

| United Kingdom | VAT | 20% Standard 20% since 4 Jan 2011, unchanged for 2026. Reduced 5% (home energy, children's car seats); zero rate on most food and children's clothes. | 5% / 0% | GOV.UK / HMRC |

Last reviewed: 2026-06-12. Need the math done for you? Pick your country in our VAT & GST calculator — the same verified rates are preloaded — then issue the invoice with the VAT invoice generator.

E-Invoicing Mandates 2026: Peppol & ViDA

The era of the "PDF Invoice" is ending. We are witnessing a global shift towards Continuous Transaction Controls (CTC).

Multiple jurisdictions are mandating E-Invoicing in 2026. This means the invoice is not a document, but a structured data file (XML, UBL, JSON) transmitted directly to tax authorities or via the Peppol network.

| Country | 2026 Mandate | Platform/Format |

|---|---|---|

| Poland | Feb 2026 (large business), Apr 2026 (most VAT-registered; micro-entrepreneurs from Jan 2027) | KSeF (National System) |

| France | Sep 2026 (receiving mandatory, large/mid sending) | Factur-X, UBL, CII |

| Belgium | Jan 2026 (B2B via Peppol) | Peppol BIS |

| Germany | Receiving since Jan 2025, sending by Jan 2027 | XRechnung, ZUGFeRD |

| Malaysia | Jan 2026 (turnover > RM1M; businesses under RM1M exempt) | MyInvois (XML/JSON) |

Prepare for ViDA (VAT in the Digital Age):

- Structured Data: Ensure your invoicing software can export to UBL 2.1 or CII standards (EN 16931).

- Real-Time Reporting: 2026 regulations often require invoices to be issued within days of the supply, not weeks.

- EU Milestone: By July 2030, all intra-EU B2B invoices must be electronic under ViDA.

Reverse Charge VAT: Cross-Border B2B Transactions

The Reverse Charge Mechanism shifts the liability to pay VAT from the supplier to the customer. This is the standard for international B2B services (e.g., a UK consultant billing a German company).

Compliance Decision Logic

For more complex cross-border scenarios involving multiple currencies, see our International Invoicing Guide or use our Multi-Currency Invoice Generator.

Common VAT Invoice Mistakes & Penalties

Auditors look for specific patterns to disallow input tax. Ensure you avoid these critical errors:

- Calculation on Gross: VAT is calculated on the Net amount. Calculating it on the Gross amount results in over/under payment.

- Invalid VRN: Using a fake or expired VAT number (especially for Reverse Charge) is considered tax fraud. Always validate foreign IDs.

- Currency Errors: For foreign currency invoices (e.g., USD invoice from a UK entity), the VAT Amount must be stated in GBP using the daily official exchange rate.

- Wrong Entity Billing: Invoices addressed to "The Group" instead of the specific legal entity holding the VAT registration will be rejected for deduction.

- Modification of Issued Invoices: You cannot simply "edit" a sent invoice. You must issue a Credit Note to cancel the original and issue a new corrected invoice. See our Credit Memo Guide for proper procedures.

Digital Services VAT: OSS & IOSS Explained

For B2C sales of digital services (SaaS, e-books, streaming) in the EU, the "Place of Supply" is the consumer's location.

- OSS (One-Stop Shop): Allows you to report all pan-EU B2C sales in a single return, rather than registering for VAT in 27 countries.

- IOSS (Import One-Stop Shop): Used for goods imported into the EU with a value under €150. This streamlines customs clearance.

- Compliance Note: Your invoice must reflect the VAT rate of the customer's country (e.g., 21% for Spain), not your own.

How to Create a VAT Invoice: Step-by-Step

Follow this strict workflow using our generator to ensure no compliance data points are missed.

- Jurisdiction & Status Verification:

Confirm the tax residency of both parties. Check valid Tax IDs.

- Input Registration Data:

Enter your VAT/GST number in the "From" field. If B2B international, the client's ID is mandatory.

- Tax Rate Assignment:

Select the correct rate per line item. Do not mix Exempt and Standard rated items without clear separation.

- Legal Notes & Annotations:

If tax is 0% (Export/Reverse Charge), select the appropriate legal disclaimer from the dropdown.

- Final Rendering:

Generate the PDF. Verify that "Tax Amount" is distinct from "Subtotal". Save for your digital records (6+ years).

If you are shipping goods internationally and need customs-compliant documentation alongside your VAT invoice, refer to our Commercial Invoice Guide and International Invoicing Guide for HS codes, Incoterms, and country-of-origin requirements.

Frequently Asked Questions About VAT Invoices

Is the supplier's VAT/GST number mandatory on an invoice?

Yes, without exception in regulated jurisdictions. According to HMRC (UK) and EU Directive 2006/112/EC, a valid VAT registration number is the primary identifier for tax deduction. Omitting this renders the document invalid for input tax recovery.

How does 'Reverse Charge' affect the invoice layout?

For Reverse Charge (B2B Cross-border), you must NOT charge VAT (0% rate). Crucially, you must include the customer's validated VAT number and a specific legal reference text stating: 'Reverse Charge applies - Customer to account for VAT'.

What is the 2026 requirement for E-Invoicing?

Multiple countries are mandating B2B e-invoicing in 2026: Poland (February/April 2026 via KSeF), France (September 2026), Belgium (January 2026 via Peppol), Germany (receiving mandatory since January 2025, sending by 2027), and Malaysia (phased through 2026 via MyInvois). This shifts from PDF invoices to structured data formats (XML/UBL) transmitted via networks like Peppol or national platforms.

What is the difference between Zero-Rated and Exempt?

Legally distinct: 'Zero-rated' goods (e.g., exports) allow you to reclaim input VAT on costs. 'Exempt' services (e.g., finance, insurance) do not allow input VAT reclamation. Misclassifying these is a common audit trigger.

What is a simplified VAT invoice?

A simplified VAT invoice is a shorter version allowed in the UK for retail sales under £250. It requires fewer details than a full VAT invoice, such as omitting the customer's name and address, while still including the supplier's VAT number and the total amount including VAT.

When do I need to issue a VAT invoice?

You must issue a VAT invoice for any taxable supply to a VAT-registered customer (B2B) within 30 days of the supply date. For B2C sales, a VAT invoice is only required if the customer requests one. The invoice must include your VAT registration number and a breakdown of the tax charged.

Where can I find the current VAT or GST rate for my country?

Use the VAT & GST Rates by Country table on this page — every standard and reduced rate is verified against the national tax authority or European Commission source linked in the same row, so you can confirm the figure before putting it on an invoice.

Do all EU countries charge the same VAT rate?

No. The EU VAT Directive only sets a floor — a minimum standard rate of 15% — and each member state sets its own rates above it, which is why standard rates across the EU range roughly from 17% to 27%. Always check the country-specific rate in the table on this page.

Disclaimer: This content is for educational and technical reference purposes. Tax legislation (VAT, GST, Sales Tax) is subject to frequent change. We recommend consulting with a chartered accountant or tax advisor for specific business rulings.